Many Philippine business owners assume that reducing their taxable income requires painstakingly tracking every receipt, invoice, and deductible expense throughout the year. This assumption makes tax season stressful and administratively heavy, particularly for small and medium enterprises (SMEs) that lack dedicated finance teams. The Optional Standard Deduction (OSD) offers a straightforward alternative: a fixed-rate deduction that sidesteps the documentation burden of itemized deductions. This article explains what OSD is, how to elect it correctly, what it changes about your compliance obligations, and how to decide whether it is the right fit for your business.

Table of Contents

Key Takeaways

| Point | Details |

|---|---|

| OSD simplifies tax filing | The optional standard deduction allows business owners to take a fixed-rate deduction, reducing paperwork compared to itemized expenses. |

| Election is time-sensitive | Choosing OSD must be done in your first quarterly return, and the choice cannot be reversed for the year. |

| Compliance duties remain | Even with OSD, you must maintain accurate records and fulfill other tax obligations, including VAT and invoicing. |

| Best fit depends on expenses | OSD benefits low-expense, high-simplification businesses, while itemized deductions may help those with higher operating costs. |

| Professional help reduces risks | Engaging advisory and bookkeeping services can help optimize tax strategy and avoid compliance pitfalls. |

What is the optional standard deduction?

The Optional Standard Deduction, commonly referred to as OSD, is a simplified method for computing deductible expenses in the Philippines. Instead of listing every actual business expense with corresponding receipts and documentation, eligible taxpayers may deduct a fixed percentage of their gross income or gross sales. This approach reduces the administrative load significantly, especially for businesses where actual deductible expenses are difficult to substantiate in full.

Under current Bureau of Internal Revenue (BIR) rules, OSD allows up to 40% deduction, but the base differs by taxpayer type. Corporate taxpayers compute OSD based on gross income — that is, gross sales or receipts less cost of sales or cost of services. Individual taxpayers, including sole proprietors and self-employed professionals, compute OSD based on gross sales or gross receipts, without deducting cost of sales first. This distinction is material: for a trading or manufacturing corporation, the OSD base after deducting COGS can be significantly smaller than gross sales. The 40% rate applies uniformly regardless of your actual expense level, which is both a strength and a limitation depending on your cost structure.

Who is eligible to use OSD?

-

Corporate taxpayers: Domestic corporations and resident foreign corporations computing regular corporate income tax may elect OSD.

-

Individual taxpayers: Self-employed individuals, sole proprietors, and professionals deriving business or professional income are also eligible.

-

General Professional Partnerships (GPPs): GPPs may elect OSD at the partnership level. However, if the GPP claims OSD, the partners can no longer claim OSD again on their distributive share of partnership income.

-

Exclusions: Purely compensation earners, non-resident aliens not engaged in trade or business, and non-resident foreign corporations are not permitted to elect OSD.

It is important to understand your tax compliance responsibilities before deciding which deduction method to adopt, because the two approaches carry distinct implications for documentation, recordkeeping, and overall tax exposure.

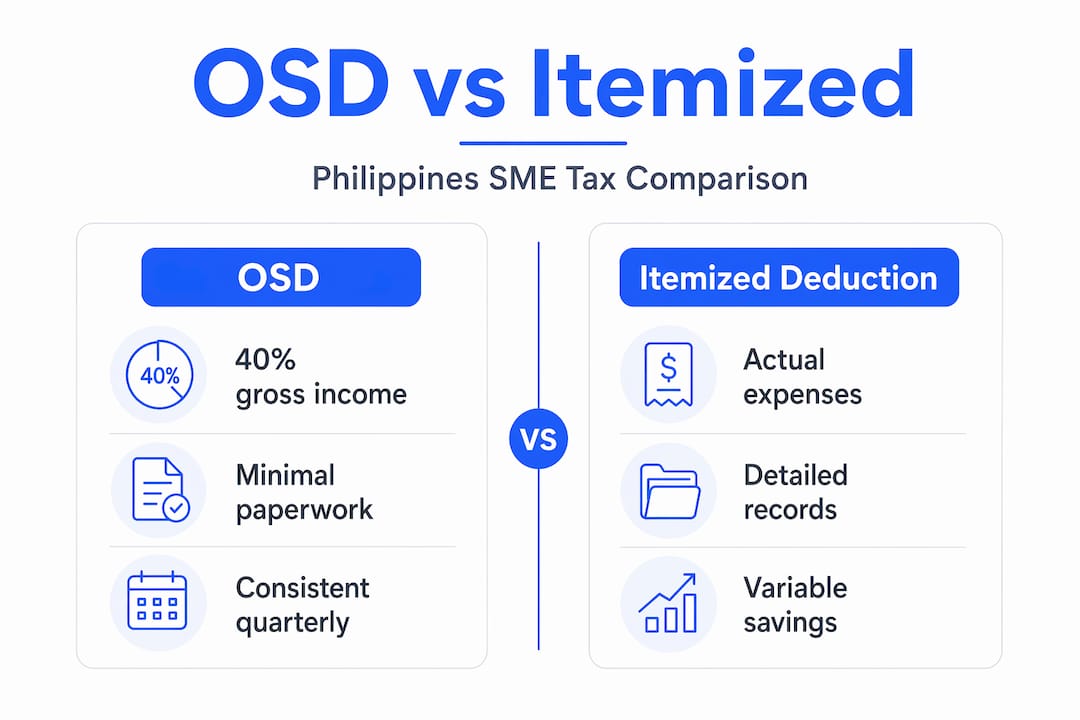

OSD vs. itemized deductions: a side-by-side comparison

| Feature | OSD | Itemized deduction |

|---|---|---|

| Deduction basis | 40% of gross income (corporations) or 40% of gross sales/receipts (individuals) | Actual allowable expenses |

| Supporting documents | Records of gross income/sales only | Full set of official receipts and invoices |

| Administrative effort | Low | High |

| Accuracy of tax deduction | Fixed, regardless of actual costs | Reflects true business expenses |

| Audit exposure on expenses | Lower | Higher if records are incomplete |

| Suitability | Low-expense or high-receipt-risk businesses | High-expense businesses with complete records |

The core trade-off is this: OSD prioritizes simplicity, while itemized deductions prioritize accuracy. Neither method is universally superior. The right choice depends on your specific cost structure and operational capacity.

How to elect OSD and why timing matters

With OSD’s basics defined, let’s move to practical steps and critical timing considerations for making your election. Many taxpayers lose the OSD privilege not because they are ineligible, but because they miss the procedural step or make the election too late in the filing cycle.

Step-by-step: how to elect OSD

-

Prepare your first quarterly income tax return for the current taxable year. For most taxpayers, this is the BIR Form 1702Q (for corporations) or BIR Form 1701Q (for individuals).

-

Check the OSD election box clearly indicated on the return. This single action formally communicates your election to the BIR.

-

Ensure the return is filed on time. Late filing of the initial quarterly return, even with OSD checked, may complicate your position during an audit.

-

Apply the 40% rate to your gross income — gross sales/receipts less cost of sales/services — for corporations, or to your gross sales/receipts for individuals, for each quarter when computing income tax due.

-

Maintain records of gross income/sales throughout the year, as these figures remain subject to BIR verification even under OSD.

-

File the annual income tax return using the same OSD basis. The election made in your first quarterly return governs the entire year.

The most critical detail here is irreversibility. Under Revenue Regulations 16-2008 (as amended by RR 2-2010), OSD is elected on the income tax return and is irrevocable for the taxable year for which it is made. Once you check that box in the first quarter, you cannot switch to itemized deductions mid-year, even if you realize your actual expenses would produce a lower tax liability.

“Electing OSD locks you in for the full taxable year. This is not a quarter-by-quarter decision.”

The consequences of failing to elect OSD properly are real. Forgetting the election can result in the loss of the benefit for that year and increased audit risk, particularly if your actual expense records are incomplete. If the BIR examines your return and finds that you attempted to use OSD without a valid election, you may face deficiency tax assessments, surcharges, and interest on the underpayment.

Pro Tip: Before the first quarterly filing deadline, compare your estimated full-year expenses against 40% of your projected gross income or sales. If your actual expenses are likely to fall below 40%, OSD will likely produce a lower taxable income for your business with significantly less paperwork. Run this estimate annually, not just in the first year you consider OSD.

Consistent bookkeeping for tax compliance throughout the year makes this comparison much easier and more reliable. Without clean books, the pre-election analysis becomes guesswork.

OSD’s impact on tax computation and compliance duties

Having covered election and timing, let’s explore how OSD tangibly changes tax reporting and compliance duties week-to-week and at filing time. A common misconception is that OSD removes most compliance obligations. In practice, it removes only one specific layer of complexity: the itemized expense documentation process.

What OSD changes:

-

You no longer need to compile and substantiate each deductible expense item for income tax computation purposes.

-

Your income tax liability is based on 60% of the applicable OSD base — gross income for corporations or gross sales/receipts for individuals — which is the portion remaining after the 40% OSD.

-

Quarterly and annual income tax filings become faster to prepare.

What OSD does NOT change:

As clearly noted in OSD recordkeeping guidance, OSD does not eliminate general compliance duties: recordkeeping, invoicing, and VAT or percentage tax obligations all remain fully in effect. This distinction matters. If your business is VAT-registered, you must still issue VAT invoices, file VAT returns, and account for input and output VAT accurately. OSD has no bearing on these obligations.

Additionally, as confirmed by guidance on journal entry requirements for OSD, OSD is a tax-only computation basis, meaning taxpayers must continue to record actual expenses in their books and reconcile gross income reporting appropriately. Your accounting books must still reflect the true financial picture of your business. The OSD adjustment happens at the tax return level, not inside your general ledger.

Expanded Withholding Tax (EWT) obligations remain fully in effect. You must still withhold the correct EWT on payments to suppliers, professionals, contractors, and lessors (e.g., 1%, 2%, 5%, 10% depending on the nature of the payment), remit it via BIR Form 0619-E monthly and BIR Form 1601-EQ quarterly, and issue BIR Form 2307 to payees. OSD only changes how you compute the income tax deduction — it does not exempt you from acting as a withholding agent.

Records you must maintain even under OSD:

-

Official receipts and sales invoices supporting gross income or gross sales figures

-

Payroll records and related documentation for employer compliance purposes

-

VAT records if applicable, including purchases and sales registers

-

Contracts, billing statements, and collection records that substantiate revenue

-

Bank statements and deposit records to corroborate gross income reported

OSD vs. itemized deduction: compliance checklist comparison

| Compliance area | OSD required | Itemized deduction required |

|---|---|---|

| Gross income/sales records | Yes | Yes |

| Expense receipts for income tax | No | Yes |

| VAT/percentage tax filings | Yes | Yes |

| Payroll and withholding | Yes | Yes |

| Books of accounts | Yes | Yes |

| Annual income tax return | Yes | Yes |

This table makes one point very clear: OSD reduces the expense documentation burden for income tax purposes only. All other compliance touchpoints remain the same. Understanding this helps you set realistic expectations when planning your accounting workload.

Quarterly reconciliation is also worth noting. Because OSD is applied each quarter based on reported gross income or sales, your finance team needs to ensure that gross income figures are accurate and consistent across all quarterly filings. Underreporting gross income to reduce OSD-computed tax creates a far more serious problem than any administrative savings would justify.

You can learn more about how tax services expertise and bookkeeping services work together to support accurate OSD-based filings across multiple business structures.

Deciding: OSD or itemized deduction for your business

With compliance clarified, let’s evaluate how to decide which route, OSD or itemized deduction, best fits your business’s unique situation. This decision is primarily financial, but it also involves administrative capacity and risk tolerance.

According to analysis of OSD versus itemized deductions, for SMEs the decision hinges on whether actual deductible expenses are less than or exceed the OSD percentage base. In plain terms: if your deductible expenses are reliably below 40% of your gross income or sales, OSD gives you a larger deduction than reality and therefore reduces your tax liability. If your actual expenses consistently exceed 40%, itemized deductions will produce a lower income tax bill.

Key factors to evaluate:

-

Actual expense ratio: Calculate your total deductible expenses as a percentage of gross income for the prior two or three years. If this ratio consistently falls below 40%, OSD is financially favorable.

-

Administrative burden: Do you have the staff and systems to maintain complete, audit-ready expense documentation? If not, the practical benefits of OSD extend beyond the tax savings themselves.

-

Receipt and invoice completeness: High-risk industries or businesses with many informal transactions may struggle to substantiate all deductible expenses. OSD reduces this exposure.

-

Business age and size: Newly established businesses often have limited historical data and higher administrative constraints. OSD can reduce the compliance burden during the early years while systems are being built.

-

VAT position: OSD does not affect input VAT claims. If your business benefits significantly from input VAT credits, a holistic review of your VAT and income tax strategy is essential before committing to OSD.

Scenarios where OSD is typically advantageous:

-

High-margin businesses where actual expenses fall well below 40% of the OSD base: For a consulting corporation with ₱10M gross income and only ₱2M in actual deductible expenses, OSD allows a ₱4M deduction instead of ₱2M under itemized — directly reducing CIT by ₱500,000 at 25% RCIT (or ₱400,000 at the 20% rate for qualified MSMEs). The more profitable the business relative to its cost base, the larger the OSD over-deduction compared to reality.

-

Service-based businesses with low direct costs, such as consulting firms, freelancers, or agencies

-

Businesses in the early growth phase with lean cost structures

-

Sole proprietors or professionals with informal or partially documented expenses

-

Businesses with inconsistent withholding tax compliance on opex: Under itemized deductions, expenses can be disallowed under Section 34(K) of the NIRC if the corresponding withholding tax was not properly withheld and remitted. OSD avoids this specific exposure for income tax purposes since the 40% deduction is not tied to individual expense items. Note: this does not eliminate the withholding tax obligation itself — the BIR can still assess deficiency withholding tax separately — but it protects the income tax deduction from being disallowed on this ground.

-

Taxpayers who have previously faced audit challenges related to expense substantiation

Scenarios where itemized deductions may be preferable:

-

Businesses with high overhead, such as manufacturing, retail, or logistics firms where actual expenses routinely exceed 40% of gross

-

Businesses with well-organized accounting teams capable of maintaining complete records

-

Companies that claim significant depreciation, interest expense, or other large deductible items not easily captured in a flat-rate formula

Pro Tip: Pull your last two years of income statements and calculate total allowable deductions as a percentage of gross income. Do this before your first quarterly filing each year. This simple exercise takes less than an hour and can save you from a suboptimal election that locks in for the full taxable year.

For businesses uncertain about which route to take, financial advisory for SMEs can provide a structured, data-driven comparison based on your specific financials, rather than relying on general rules of thumb.

Why streamlined deductions alone don’t future-proof your business

OSD is a genuinely useful tool, but it is frequently misunderstood as a complete tax optimization strategy. It is not. It is a method for computing one component of one tax obligation: income tax. Treating OSD as a comprehensive solution to your tax and compliance workload creates a false sense of security that can be costly over time.

The most common mistake we observe is businesses adopting OSD primarily to avoid maintaining detailed books. This approach creates two problems. First, the underlying books remain disorganized, which affects decision-making, financial reporting, and audit readiness for all other tax types. Second, when the BIR audits gross income, incomplete records leave the taxpayer unable to substantiate the revenue figures that form the basis of the OSD computation itself. You have reduced receipt risk but not eliminated income verification risk.

As confirmed by guidance on OSD and broader compliance, OSD selection impacts only income tax computation and full optimization requires holistic planning. This is a point worth emphasizing for any growing business. Your tax exposure does not begin and end with income tax. VAT, withholding tax, and local business tax all require separate, accurate compliance tracks.

Another consideration is regulatory change. The Philippine tax environment has seen significant reform in recent years, and the rules governing OSD eligibility, rates, and election procedures can be amended. Businesses that rely on a set-and-forget approach to OSD risk non-compliance when the regulatory context shifts. Proactive engagement with your finance and tax advisors, supported by robust finance and accounting expertise, positions your business to adapt quickly rather than scrambling to catch up after a BIR issuance or administrative audit.

The long-term view is clear: OSD is a valid, efficient election for the right type of business, but it works best when embedded within a broader compliance and planning framework, not used as a substitute for one.

Make tax compliance easier with expert support

Choosing between OSD and itemized deductions is just one decision in a broader tax compliance landscape. Getting it wrong has consequences that carry through the full taxable year.

Proseso Consulting works with Philippine SMEs and startups to build clean, audit-ready books and navigate the annual OSD election with confidence. Whether you need reliable bookkeeping support to maintain accurate gross income records or structured guidance on your overall finance and accounting services, we provide end-to-end support that simplifies compliance without cutting corners. Our cloud-based approach means your records are organized, accessible, and ready for any BIR review, so tax season becomes a process rather than a crisis.

Frequently asked questions

Can I switch between OSD and itemized deductions within the same year?

No. Once OSD is elected in your first quarterly income tax return, the choice binds you for the entire taxable year. Plan the decision carefully before that first filing.

Does OSD cover VAT obligations in the Philippines?

No, OSD impacts income tax computation only, and as confirmed by BIR compliance rules, VAT rules and all related documentation requirements must still be met separately.

What records must I keep when using OSD?

You must maintain accurate records supporting your gross income or sales figures, including official receipts, invoices, and bank records, even though expense documentation for income tax purposes is not required.

Is OSD beneficial for businesses with high expenses?

If your actual deductible expenses consistently exceed 40% of your gross income, itemized deductions may produce a lower tax liability than OSD because the actual expense total would exceed the fixed 40% deduction.

What happens if I forget to elect OSD?

You may lose the privilege for that tax year and face audit risk on all expenses, with deficiency tax exposure if your supporting receipts and documentation are insufficient to substantiate itemized deductions.