Many Filipino entrepreneurs are paying more taxes than they legally need to. If you operate as a sole proprietor under graduated rates, your business income can climb to a 35% marginal rate once net taxable income exceeds PHP 8,000,000. Registering a corporation locks in a flat 20% or 25% corporate income tax rate, which becomes significantly more favorable as income grows past the PHP 3,000,000 VAT threshold. Below that threshold, the 8% optional flat tax often remains the best choice — but past it, corporate registration is usually where the real tax savings live. This guide walks through the exact comparison, practical examples, registration steps, and compliance requirements you need to act on this.

Table of Contents

-

Key Takeaways

-

How sole prop vs. corporate tax rates compare

-

Real tax savings examples by income level

-

How to register a company and comply with BIR rules

-

Additional tax incentives only corporations can access

-

Staying compliant after registration to protect your savings

-

What corporate registration actually changes for Filipino entrepreneurs

-

How Proseso-consulting helps you register and optimize taxes

-

FAQ

Key Takeaways

| Point | Details |

|---|---|

| Corporate vs. sole prop tax rates | Corporations pay a flat 20% or 25% rate, while sole proprietors face graduated rates up to 35%. |

| Income threshold matters | For sole proprietors above the PHP 3M VAT threshold, the corporate tax advantage becomes clear once net taxable income exceeds PHP 2,000,000. Below the VAT threshold, the 8% flat tax option is usually more efficient than incorporating. |

| BIR registration is time-sensitive | BIR registration must be completed before commencing business operations, with DST on the original issuance of shares due within 5 days after the close of the month of share issuance. |

| PEZA and incentive access | Registered corporations can access tax holidays and reduced rates unavailable to sole proprietors. |

| Compliance is non-negotiable | Even zero-income corporations must file nil returns or risk penalties and blocked tax clearances. |

How sole prop vs. corporate tax rates compare

The single most important number in this conversation is the tax rate applied to your net income. Under Philippine tax law, corporate tax rates versus individual rates differ sharply: corporations pay a flat 20% (for domestic corporations with net taxable income not exceeding PHP 5,000,000 and total assets not exceeding PHP 100,000,000, excluding land) or 25% for larger entities, while sole proprietors are taxed on a graduated schedular scale.

Here is what the graduated scale looks like for a sole proprietor under the Tax Reform for Acceleration and Inclusion (TRAIN) Law, applying the rates effective from January 1, 2023 onwards:

| Annual Net Taxable Income (PHP) | Tax Rate |

|---|---|

| 0 to 250,000 | 0% |

| 250,001 to 400,000 | 15% on excess over 250,000 |

| 400,001 to 800,000 | PHP 22,500 + 20% on excess over 400,000 |

| 800,001 to 2,000,000 | PHP 102,500 + 25% on excess over 800,000 |

| 2,000,001 to 8,000,000 | PHP 402,500 + 30% on excess over 2,000,000 |

| Over 8,000,000 | PHP 2,202,500 + 35% on excess over 8,000,000 |

Sole proprietors and professionals whose annual gross sales or receipts do not exceed the PHP 3,000,000 VAT threshold may also elect the 8% flat tax option under Section 24(A)(2)(b) of the Tax Code. This option applies 8% to gross sales or receipts in excess of PHP 250,000, in lieu of both the graduated income tax rates and the 3% percentage tax. For sole proprietors below the VAT threshold, the 8% option is frequently more tax-efficient than either graduated rates or corporate registration. This comparison becomes most relevant once you exceed the PHP 3,000,000 VAT threshold, where the 8% option is no longer available and the graduated rates apply by default.

Once you exceed the PHP 3,000,000 VAT threshold and the 8% option is no longer available, the graduated rates kick in for sole proprietors. At PHP 2,000,001 net taxable income and beyond, the marginal personal rate hits 30%. A corporation paying a flat 20% rate at that same income level is already ahead. Choosing the right business structure is not just a legal formality; it directly determines how much of your earnings you keep.

Pro Tip: If your gross sales exceed the PHP 3,000,000 VAT threshold and your net taxable income consistently exceeds PHP 2,000,000 per year, run a side-by-side tax calculation using the corporate rate. The savings often justify the registration cost within the first year. Below the VAT threshold, the 8% flat tax election usually outperforms incorporation on tax grounds alone.

Both corporations and sole proprietors deduct ordinary and necessary business expenses under Section 34(A) — employee benefits, depreciation, rent, utilities, and certain pre-operating costs. The deduction itself is not a corporate advantage; a sole proprietor claims the same itemized expenses. Alternatively, either structure may elect the 40% Optional Standard Deduction (OSD) in lieu of itemizing, though the base differs: for individuals the 40% is taken on gross sales or receipts, while for corporations it is taken on gross income (gross sales less cost of sales or services). Where a corporation does hold an edge is structural — the documentation standards and ability to formalize expenses like director fees and salaries make aggressive but defensible expense recognition more practical.

Real tax savings examples by income level

Numbers make this concrete. Below are three scenarios comparing the tax burden across the three main options: a sole proprietor under graduated rates, a sole proprietor electing the 8% flat tax (where eligible), and a domestic small corporation eligible for the 20% rate. For the 8% scenarios, we assume gross sales equal the net taxable income figure plus PHP 250,000 of allowable deductions for illustration; in practice, the 8% is computed on gross receipts in excess of PHP 250,000, regardless of expenses.

-

Scenario A: PHP 500,000 net taxable income (PHP 750,000 gross). Sole proprietor under graduated rates pays PHP 22,500 plus 20% of the PHP 100,000 excess over PHP 400,000, totaling PHP 42,500. Sole proprietor under the 8% option pays 8% of (PHP 750,000 − PHP 250,000), totaling PHP 40,000. Corporation at 20% pays PHP 100,000. The 8% option wins at this level, with the graduated sole prop close behind. Corporate registration is not yet the tax play here — but this is the low end, and the picture changes quickly as income grows.

-

Scenario B: PHP 1,500,000 net taxable income (PHP 1,750,000 gross, still below VAT threshold). Sole proprietor under graduated rates pays PHP 102,500 plus 25% of the PHP 700,000 excess over PHP 800,000, totaling PHP 277,500. Sole proprietor under the 8% option pays 8% of (PHP 1,750,000 − PHP 250,000), totaling PHP 120,000. Corporation at 20% pays PHP 300,000. The 8% option dominates by a wide margin while you remain below the VAT threshold. But this is the last income level where staying a sole proprietor clearly pays off — the moment gross sales cross PHP 3,000,000 and the 8% election disappears, the comparison flips sharply toward incorporation, as Scenario C shows. Even here, the corporation already adds liability protection and access to incentives the 8% election cannot offer.

-

Scenario C: PHP 3,000,000 net taxable income, modeled as a high-margin business (gross only modestly above the VAT threshold, so most of gross flows to net; the 8% option is no longer available). This is where many growing businesses land once revenue scales and margins hold up.

Sole proprietor under graduated rates pays PHP 402,500 plus 30% of the PHP 1,000,000 excess over PHP 2,000,000, totaling PHP 702,500. Corporation at 20% pays PHP 600,000. That is a savings of PHP 102,500 in one tax year alone, and at this gross level both structures become VAT-registrable, so 12% VAT now applies on sales rather than the 3% percentage tax under Section 116 — a consequence of crossing the threshold, not of incorporating (though VAT is generally passed through to customers and recoverable on input VAT). At the 25% corporate rate (for larger entities), the tax is PHP 750,000, which is still lower than the graduated rate effect compounded across a growing sole proprietorship income. One caveat the flat-rate comparison hides: the 20% corporate rate is only the first layer. When the owner extracts profit as dividends, a 10% final withholding tax applies on the distribution to a resident individual (25% for a non-resident foreign owner, often reducible under a tax treaty). A sole proprietor faces no such second layer — after-tax profit is already personal money. The practical takeaway favors incorporation for a growing business: profit kept inside the company to fund expansion is taxed just once at 20%, with the dividend layer applying only if and when you choose to pull cash out. For owners reinvesting in growth — which is most scaling businesses — the full rate advantage stays intact year after year.

The pattern is clear. Below the PHP 3,000,000 VAT threshold, the 8% flat tax on gross receipts is usually the most tax-efficient option for sole proprietors. Once a business crosses the VAT threshold, the 8% option disappears and the comparison becomes graduated rates vs. corporate registration. At that point, corporate registration starts delivering clear tax savings, and the gap widens consistently each year. Additionally, corporations can structure director fees, salaries, and dividends in ways that further reduce the overall tax burden on the business owner, which sole proprietors cannot replicate. High-margin businesses benefit most from incorporating. A consulting, software, or service business with low cost of sales keeps most of its gross as net taxable income — and that is precisely where the flat 20% corporate rate pulls furthest ahead of the 30% graduated bracket. Such businesses can also elect the 40% OSD to simplify compliance while locking in the lower corporate rate, capturing the rate advantage without the burden of substantiating every expense. The higher your margins and the more your income grows, the stronger the case for corporate registration.

How to register a company and comply with BIR rules

The registration process is sequential and has strict deadlines attached at each step.

-

Step 1: Choose your business structure. Most entrepreneurs choose between a regular domestic corporation (minimum of two incorporators under the Revised Corporation Code, reduced from the previous minimum of five under the old Corporation Code) and a One Person Corporation (OPC), which allows a single stockholder. The OPC is particularly attractive for solo entrepreneurs who want corporate tax treatment without co-founders. Note that the SEC prohibits certain regulated professionals — including lawyers, doctors, and CPAs — from forming OPCs to practice their profession; these professionals must use a regular professional partnership or corporation instead.

-

Step 2: Reserve your company name with the SEC. Use the SEC’s online portal, the Electronic Simplified Processing of Applications for Registration of Companies (eSPARC) system, to check name availability and reserve it.

-

Step 3: Prepare and file incorporation documents. These include the Articles of Incorporation, By-Laws, Treasurer’s Affidavit, Sworn Statement of the Treasurer, and the cover sheet. For an OPC, the requirements are slightly simplified. Submit via eSPARC for faster processing.

-

Step 4: Register with the BIR before commencing business operations. Under Section 236 of the Tax Code, BIR registration must be completed before you start operating, issue any official invoice, or hire employees. A related and time-sensitive obligation is the payment of Documentary Stamp Tax on the original issuance of shares under Section 175 of the NIRC. The DST return (BIR Form 2000-OT) must be filed and paid within five days after the close of the month in which the shares were issued, which typically coincides with the month of SEC incorporation. Late registration or late DST payment exposes the company to compromise penalties under Section 275 of the NIRC, plus a 25% surcharge and 12% annual interest on any tax due. You will obtain your Tax Identification Number (TIN) and Certificate of Registration (BIR Form 2303) at this stage. Once the COR is issued, you have 30 days to apply for Authority to Print invoices and receipts.

-

Step 5: Register your books of accounts and Authority to Print receipts. The BIR requires corporations to maintain officially registered accounting books and to have their official receipts and invoices authorized before use.

-

Step 6: Enroll in BIR’s electronic filing and payment system (eFPS or eBIRForms). Large taxpayers are mandated to use eFPS. Most SMEs use eBIRForms for electronic submission.

| Registration Step | Key Requirement | Deadline |

|---|---|---|

| SEC incorporation | Articles of Incorporation, OPC or regular corp documents | Upon formation |

| BIR registration | TIN, BIR Form 1903, Certificate of Registration | Before commencing business operations |

| Books of accounts | General ledger, journal, subsidiary books | Before commencing operations |

| Authority to Print | BIR-accredited printer for receipts and invoices | Before issuing any invoice |

Pro Tip: DIY BIR registration is possible, but a missed form, wrong tax type election, or incorrect RDO assignment can open a case that takes months to resolve and often costs more than the advisory fee itself. Most entrepreneurs find professional guidance pays for itself within the first compliance cycle.

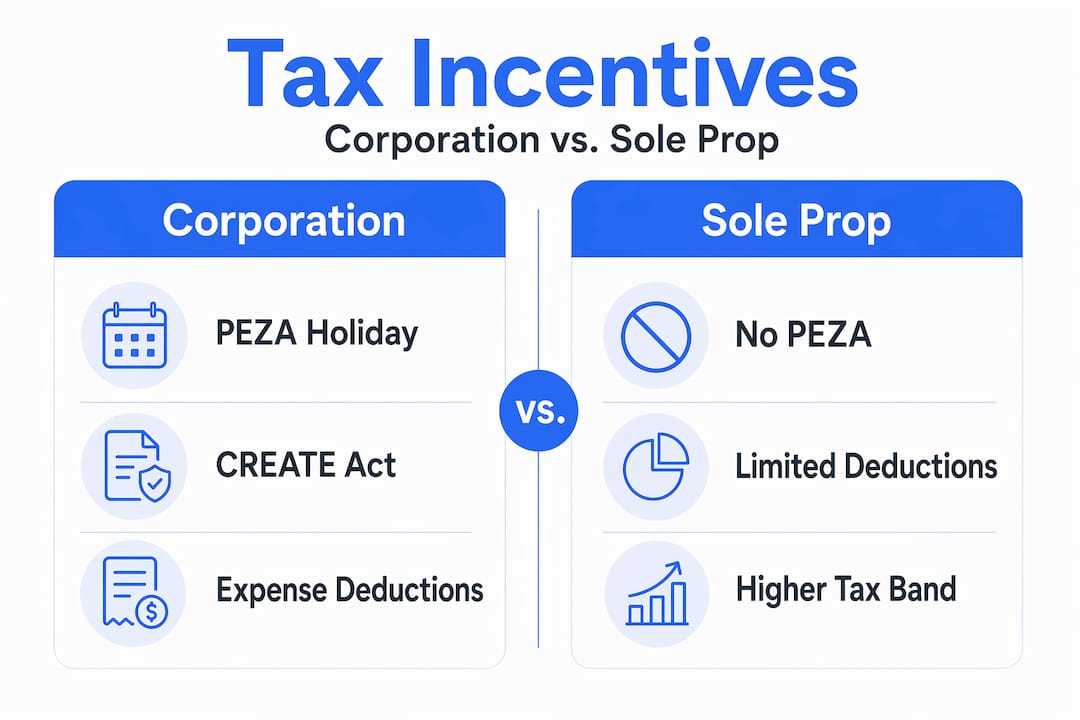

Additional tax incentives only corporations can access

Beyond the flat income tax rate, registered corporations unlock a category of tax benefits that sole proprietors simply cannot reach.

PEZA-registered export enterprises receive an Income Tax Holiday for four to seven years, during which corporate income tax is zero. After the ITH period, export enterprises can elect either a 5% Special Corporate Income Tax (SCIT) on Gross Income Earned in lieu of all national and local taxes, or the Enhanced Deductions Regime (EDR) at a 20% corporate income tax rate, for up to 10 years. For a technology company or export-oriented manufacturer, this incentive alone can generate millions of pesos in tax savings over a decade.

| Incentive Type | Who Qualifies | Tax Benefit |

|---|---|---|

| PEZA Income Tax Holiday | PEZA-registered export enterprises | 0% income tax for 4 to 7 years |

| PEZA Post-ITH Regime | Post-ITH PEZA export enterprises | 5% SCIT on Gross Income Earned OR 20% CIT with Enhanced Deductions, for 10 years |

| VAT zero-rating | PEZA and BOI-registered exporters | 0% VAT on local purchases |

| CREATE Act reduced rates | Domestic corps with assets below PHP 100M | 20% corporate income tax rate |

| CREATE MORE Enhanced Deductions Regime | RBEs registered with an IPA electing the EDR | 20% corporate income tax with enhanced deductions on labor, training, R&D, and power expenses |

The Corporate Recovery and Tax Incentives for Enterprises (CREATE) Act, as amended by the CREATE MORE Act (RA 12066, signed in November 2024), introduced a system of performance-based incentives administered through the Fiscal Incentives Review Board (FIRB), giving registered corporations structured pathways to reduced tax obligations tied to investment commitments. CREATE MORE further lowered the corporate income tax rate to 20% for Registered Business Enterprises under the Enhanced Deductions Regime, expanded VAT zero-rating and duty-free privileges, and extended the maximum incentive period to up to 17 or 27 years depending on the approving authority. None of these pathways are available to a sole proprietor operating outside a registered legal entity.

Staying compliant after registration to protect your savings

Registering your company is only the beginning. Protecting the tax advantages of company registration for tax optimization requires consistent compliance on multiple fronts.

-

All corporations must file annual income tax returns (BIR Form 1702) and quarterly income tax returns (BIR Form 1702Q), regardless of whether the company earned any income during the period.

-

Even a newly formed corporation with zero revenue must file nil returns. Failure to do so results in open cases at the BIR, which can block future tax clearance certificates and delay business transactions.

-

Keeping BIR registration updated is mandatory whenever your business address, tax type, or registration status changes. Outdated registration leads to penalties, administrative holds, and difficulty securing clearances.

-

Non-compliance penalties accumulate through surcharges of 25% or 50% on unpaid taxes, compromise penalties, and interest at 12% per annum. These amounts add up quickly when open cases go unresolved for multiple tax years.

-

Maintain complete books of accounts, official receipts, and supporting documentation for at least ten years. The BIR can audit transactions going back several years, and missing records shift the burden of proof to the taxpayer.

Pro Tip: Engaging a bookkeeping and tax compliance service from day one of your corporation’s life removes the risk of missed filings and accumulating penalties. Think of it as the operational cost that protects every other tax benefit you registered for.

What corporate registration actually changes for Filipino entrepreneurs

Many business owners make the same calculation: “Staying as a sole proprietor is simpler.” The logic is understandable. Setting up a corporation feels like adding paperwork and cost to an already stretched operation.

But the pattern across hundreds of growing Philippine businesses tells a different story. Entrepreneurs who delay corporate registration are not just paying higher taxes today. They are also missing the deduction categories, the credibility with banks and suppliers, and the legal protection that a registered entity provides. By the time the tax burden becomes painful enough to act on, significant money has already been left on the table across multiple tax years.

The switch from schedular taxation to a flat 20% corporate rate is not just a number change on a return. It changes how the business budgets, how it plans for growth, and how it approaches expense management. Once the effective tax rate is capped, business finances can be modeled with far more precision.

The strongest takeaway: do not wait until you are already deep in a high-income year to register. File early, get the bookkeeping and tax compliance setup in place, and use the corporate structure intentionally from the start. The registration fee is trivial compared to the compounding advantage of lower tax rates applied consistently over years of growth.

How Proseso-consulting helps you register and optimize taxes

Running a business is demanding enough without having to track SEC deadlines, BIR form numbers, and filing windows simultaneously.

Proseso-consulting handles the end-to-end process for entrepreneurs ready to make the move to corporate registration. From preparing your Articles of Incorporation and OPC documents to registering with the BIR, setting up your books of accounts, and managing your quarterly and annual tax filings, the firm takes compliance off your plate. The team also provides ongoing CFO advisory services to help you structure compensation, dividends, and deductible expenses in ways that fully maximize the tax benefits of your corporate status. If you are serious about keeping more of what you earn, the conversation starts here.

FAQ

What income level makes corporate registration worth it for tax purposes?

Once you cross the PHP 3,000,000 VAT threshold — where the 8% flat tax option is no longer available — corporate registration delivers a clear and growing tax advantage. Above PHP 2,000,000 in annual net taxable income, the sole proprietor’s marginal rate hits 30%, while a qualifying corporation pays a flat 20%, and that gap widens every year as income grows. The advantage is strongest for high-margin businesses and for owners who reinvest profit, since earnings kept in the company are taxed just once at 20%. A couple of practical notes: both structures deduct the same business expenses or may elect the 40% OSD, so it’s your net figure that drives the comparison; and a 10% dividend tax applies only if and when you distribute profit to yourself. Below the VAT threshold, the 8% flat tax usually remains the more efficient route until you scale past it.

How long does it take to register a company with the SEC and BIR in the Philippines?

SEC registration via eSPARC typically takes one to three weeks depending on document completeness. BIR registration must be completed before commencing business operations, issuing official invoices, or hiring employees. Late registration exposes the company to compromise penalties, a 25% surcharge, and 12% annual interest on unpaid taxes.

Can a One Person Corporation (OPC) qualify for the 20% corporate tax rate?

Yes. An OPC is treated as a domestic corporation under Philippine tax law and qualifies for the 20% flat corporate income tax rate if net taxable income does not exceed PHP 5,000,000 and total assets excluding land are below PHP 100,000,000.

What happens if a corporation fails to file a return when it has zero income?

Corporations with zero income must still file nil returns with the BIR. Failure to do so results in open cases, penalty surcharges, and blocked tax clearance certificates that can disrupt future business operations.

What is the PEZA Income Tax Holiday and who qualifies?

PEZA-registered export-oriented companies receive an Income Tax Holiday of four to seven years with zero corporate income tax. After the ITH, export enterprises can elect either a 5% Special Corporate Income Tax (SCIT) on Gross Income Earned in lieu of all national and local taxes, or the Enhanced Deductions Regime at a 20% corporate income tax rate, for up to 10 years.