For many SMEs in the Philippines and Singapore, the monthly close is a recurring source of stress: late reports, reconciliation errors, missed accruals, and last-minute scrambles before tax filings. The 7-step monthly closing process every growing SME should adopt addresses these problems directly by replacing ad-hoc habits with a structured, repeatable framework. When executed consistently, this process improves financial accuracy, reduces audit risk, and gives business owners the reliable data they need to make sound decisions each month.

Table of Contents

-

Key takeaways

-

Prerequisites for an effective monthly close

-

The 7-step monthly closing process

-

Modernizing the close: automation and live accounting

-

Common mistakes and how to avoid them

-

Measuring success and improving over time

-

Why most SME closes fail

-

How Proseso-consulting supports your monthly close

-

FAQ

Key takeaways

| Point | Details |

|---|---|

| Start with preparation | A published close calendar with assigned ownership prevents the most common bottlenecks before they start. |

| Reconcile before you adjust | Completing reconciliations before posting adjusting entries catches errors at the source, not after the fact. |

| Period lock protects integrity | Locking the accounting period after approval prevents ad-hoc changes that compromise your audit trail. |

| Retrospectives drive improvement | A short post-close review each month compounds into significantly fewer errors and faster closes over time. |

| Process beats skill | Most close failures trace back to missing process architecture, not the competence of the finance team. |

| Automation reshapes the close | Modern accounting platforms automate AP capture, bank reconciliation, AR follow-ups, and recurring entries — making live accounting and faster closes achievable for SMEs. |

Prerequisites for an effective monthly close

Before you execute any step in the closing process, your organization needs two things in place: clear ownership and reliable data sources. Without these, even the most detailed monthly closing checklist will stall.

What you need before day one

The foundation of an effective monthly close is a published close calendar that specifies cutoff dates for each transaction type. Accounts payable cutoffs, payroll submission deadlines, and expense report submission windows should all be documented and communicated to every department that feeds data into finance. Incomplete upstream data and unclear cutoff ownership are consistently the biggest bottlenecks in month-end close operations.

Beyond the calendar, assign explicit ownership for each closing task. Finance managers should know who is responsible for bank reconciliations, who handles intercompany eliminations, and who reviews payroll journals. Ambiguity in ownership is a direct cause of delays.

Your essential data sources for a complete close include:

-

Accounts payable (AP) subledger with all vendor invoices and payment records through the cutoff date

-

Accounts receivable (AR) aging report with collections activity and credit notes

-

Payroll register finalized and approved before the close window opens

-

Bank and credit card feeds imported and matched through the last day of the period

-

Expense reports submitted and coded by department

| Requirement | Owner | Deadline |

|---|---|---|

| Close calendar published | Finance Manager | 5 days before period end |

| AP cutoff enforced | AP Specialist | Last business day of month |

| Payroll finalized | HR / Payroll Lead | 2 days before period end |

| Bank feeds imported | Bookkeeper | Day 1 of close window |

| Expense reports submitted | All department heads | Last business day of month |

Pro Tip: Use a shared close tracker (a simple spreadsheet or a task module in your accounting system) where each owner marks their item complete. This single change eliminates the most common cause of close delays: not knowing what is still open.

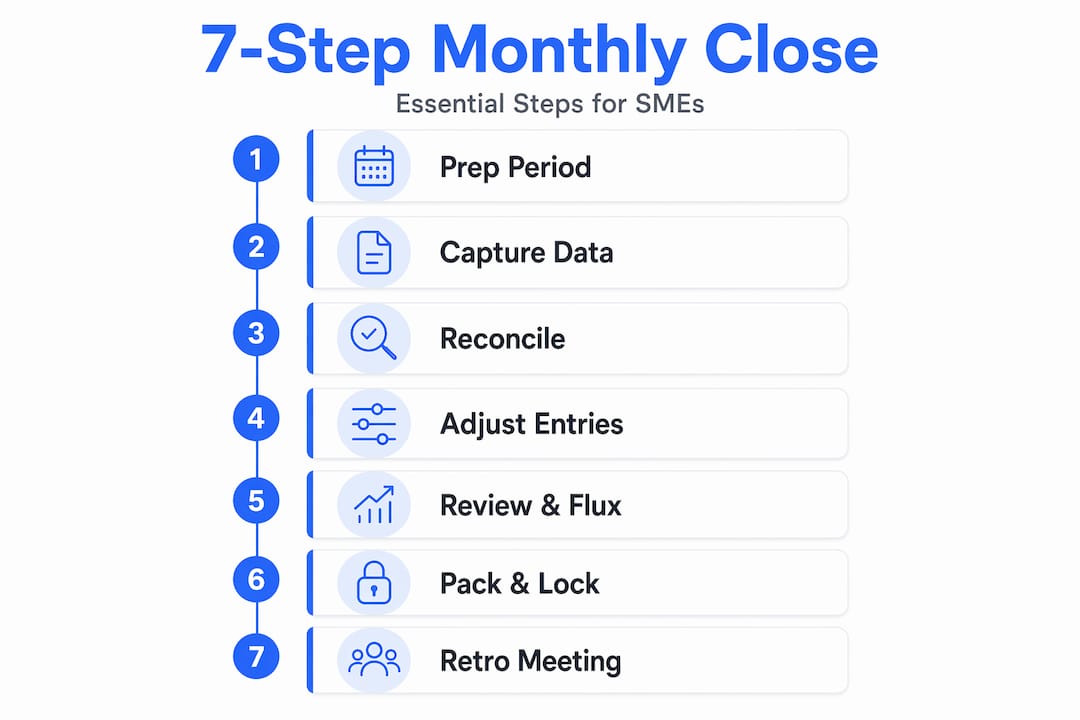

The 7-step monthly closing process

A practical 7-step month-end close includes pre-close preparation, transaction capture, reconciliations, adjusting entries, account review, approvals with period lock, and a post-close retrospective. Each step has defined outputs and evidence requirements that make the process repeatable regardless of who executes it.

Step 1: Pre-close preparation

Review the open items log from the prior month to check whether any unresolved items carry forward. Distribute the close calendar to all stakeholders and confirm receipt. This step takes less than two hours but prevents the confusion that derails closes in their first 24 hours.

Step 2: Transaction capture and source data completion

Import all bank and credit card feeds. Post all vendor invoices received through the cutoff. Confirm that payroll journals have been recorded and that all employee expense reports are coded and approved. The goal is a complete, unambiguous transaction record before any reconciliation begins. Any invoice or expense submitted after the cutoff belongs to the next period.

Step 3: Reconciliations

This is the most evidence-intensive step. Reconcile every balance sheet account against its supporting source: bank statements against the general ledger, AR subledger against the control account, AP subledger against the control account, and payroll liability accounts against the payroll register. For any discrepancy, document the nature of the difference, the responsible owner, and the resolution status before moving forward.

Pro Tip: Standardized reconciliation templates that document balances, differences, and explanations in a consistent format reduce reviewer time significantly and improve audit readiness. Build these once and reuse them every month.

Step 4: Adjusting entries, accruals, and deferrals

Post all supported adjusting entries: accrued expenses for services received but not yet invoiced, deferred revenue for payments received in advance, depreciation and amortization, and prepaid expense amortization. Every adjusting entry must reference a supporting document. An accrual without a contract, delivery receipt, time record, or calculation sheet is not a supported entry. Unsupported entries are one of the most common reasons auditors raise findings against SME financial statements.

Step 5: Account-level review and flux analysis

Review every income statement line and significant balance sheet account against the prior month and the prior year equivalent period. Flag any movement greater than a defined threshold (for example, 10% or a fixed dollar amount) and document the business reason. This step catches posting errors, duplicate entries, and misclassifications before the financials reach management. A flux analysis does not need to be complex. A simple table with prior period, current period, variance, and explanation columns is sufficient.

Step 6: Approvals, financial packaging, and period lock

Prepare the financial package: income statement, balance sheet, cash flow statement, and supporting schedules. Obtain sign-off from the authorized reviewer, typically the CFO, Finance Manager, or business owner. Once approved, lock the accounting period. A period lock serves as a control boundary: any post-close change requires a documented approval and creates an audit trail. This control prevents ad-hoc adjustments that compromise the integrity of reported figures.

Step 7: Post-close retrospective

Within two business days of completing the close, hold a brief review with the finance team. Log every issue that caused a delay or required a correction, identify the root cause, and assign a process change to prevent recurrence. This step is where the SME financial process matures over time.

| Step | Key Output | Control Objective |

|---|---|---|

| Pre-close prep | Open items log, confirmed cutoffs | Completeness |

| Transaction capture | Fully posted transaction record | Completeness, cutoff |

| Reconciliations | Signed reconciliation workpapers | Accuracy, authorization |

| Adjusting entries | Supported journal entries | Accuracy, authorization |

| Account review | Flux analysis with explanations | Accuracy, reasonableness |

| Approvals and lock | Approved financials, locked period | Authorization, auditability |

| Retrospective | Issue log, updated standards | Continuous improvement |

Modernizing the close: automation and live accounting

The 7-step framework above is the operational backbone, but it does not have to be executed manually and monthly the way most SMEs still execute it today. The most disciplined finance teams in Singapore and the Philippines have moved to a live accounting model, where automation handles routine work throughout the month and the period-end exercise becomes a verification rather than a sprint.

Live accounting treats the books as a real-time system, not a periodic event. Transactions are captured, coded, and reconciled as they happen, supported by automation. For businesses with high transaction volumes — e-commerce, retail, distribution, BPO — a weekly or daily soft close delivers materially better management information and reduces the month-end workload. The hard close at month-end becomes a confirmation step rather than a discovery exercise.

Modern accounting platforms — Odoo, Xero, QuickBooks Online, and similar — now offer automation at every step of the close:

-

AP bill capture: OCR and AI tools like Odoo’s built-in OCR, Dext, and Hubdoc extract vendor, amount, date, and tax code automatically from invoices, reducing manual AP entry by 80% or more.

-

Bank feed integrations: Direct connections between your accounting system and your bank import transactions in near real time, eliminating manual CSV uploads. Most major banks in the Philippines and Singapore now support direct feeds.

-

Suggestive reconciliation: Systems like Odoo automatically suggest matches between bank transactions and open invoices, shifting the bookkeeper’s role from data entry to exception review.

-

AR automation: Automated reminders, dunning sequences, and embedded payment links accelerate collections and keep AR aging accurate.

-

Scheduled recurring entries: Depreciation, amortization, prepaid expense releases, and accruals can be scheduled in advance and posted automatically at period end.

-

Intercompany matching: For SMEs with multiple entities — common for businesses operating across Philippines and Singapore — automated IC matching removes one of the most error-prone manual tasks from the close.

Two further practices separate well-run modern closes from the rest:

-

First, pre-close exception reports surface unposted transactions, unreconciled bank items, and unapproved expense reports several days before period end — turning the close from a discovery exercise into a confirmation one.

-

Second, approved close data feeds into always-on dashboards (Odoo’s native reporting, Power BI, Metabase, Fathom) that business owners consult throughout the month, rather than waiting for the PDF financial package five to seven days after period end.

Pro Tip: Automation does not replace the 7 steps. It changes how each step is executed. The control objectives — completeness, accuracy, authorization, cutoff, auditability — remain the same. The goal is to remove manual effort from the work that does not require judgment, freeing the finance team to focus on the work that does.

Common mistakes and how to avoid them

Even well-intentioned finance teams repeat the same errors month after month. Most of these errors are preventable with the right controls.

The most frequent problem is inconsistent cutoff enforcement. When one department submits invoices three days after the cutoff and finance accepts them anyway, the close extends, and the prior month’s figures shift. The fix is a written policy: invoices received after the cutoff date are recorded in the following period, with no exceptions without documented approval from the Finance Manager.

A second common failure is late or unsupported adjusting entries. Accruals posted without supporting documentation create audit exposure and, in regulated markets like Singapore and the Philippines, can trigger compliance findings. Each adjusting entry should carry a reference number tied to a supporting file.

Unclear ownership is a structural problem, not a personnel problem. When two people each assume the other is handling the intercompany reconciliation, it does not get done. Assign one owner per task. That person is accountable for completion, even if they delegate the execution.

Additional controls that reduce bottlenecks:

-

Review gates: Require reconciliations to be signed off before adjusting entries are posted. Require adjusting entries to be approved before the financial package is prepared.

-

Automation for transaction matching: Use your accounting system’s bank feed matching rules to auto-match routine transactions, reserving manual review for exceptions only.

-

Document storage: Attach supporting files directly to journal entries and reconciliations in your accounting system so reviewers can access evidence without requesting it separately.

-

Segregation of duties: The person who posts a journal entry should not be the same person who approves it. For small teams, this may mean the business owner approves entries above a defined threshold.

Pro Tip: Strong financial controls for SMEs combine clear roles, regular checks, and targeted automation. You do not need a large team to achieve this. You need a documented process and the discipline to follow it.

Measuring success and improving over time

A monthly closing checklist tells you what to do. Key performance indicators tell you how well you are doing it. Track these metrics every month:

-

Close cycle time: The number of business days from period end to approved financial package. A target of five to seven business days is achievable for most SMEs.

-

Discrepancies identified and resolved: Count the number of reconciling items found each month and track whether the number is trending down over time.

-

Adjusting entries requiring revision: If entries are frequently revised after initial posting, the root cause is usually insufficient review of supporting documentation before posting.

-

Audit findings or queries: Any question from an external auditor or tax authority that traces back to the close process is a signal that a control needs strengthening.

-

Repeat issues from the retrospective log: If the same problem appears in three consecutive retrospectives, the process change assigned to address it has not been effective.

The post-close retrospective is the mechanism that converts these metrics into process improvements. Review the issue log, confirm that prior action items were completed, and update your close calendar, templates, or ownership assignments accordingly. Data-driven adjustments to your business closing procedures compound over time. A team that runs a disciplined retrospective every month will close faster and with fewer errors in month twelve than it did in month one. The annual compliance checklist from Proseso-consulting is a useful reference for aligning your monthly process with broader regulatory requirements across Southeast Asia.

Why most SME closes fail

Across finance teams in the Philippines and Singapore, the pattern is consistent. When a monthly close goes wrong, the instinct is to blame the team. The actual cause is almost always missing process architecture.

Month-end close failure typically stems from poor process architecture, not team skill. Experienced accountants frequently produce unreliable financials month after month simply because no one had ever defined what a complete close looked like or who owned each piece of it. The moment a published calendar, assigned ownership, and a documented evidence requirement for every entry are introduced, the same team produces materially better results.

Two controls are non-negotiable: the period lock and the retrospective. The period lock is not bureaucracy. It is the line between financial data you can rely on and financial data that might have changed since you last looked at it. The retrospective is not a meeting for its own sake. It is the only mechanism that prevents a team from solving the same problem twelve times a year.

Separating duties matters more than most SME owners realize. When the same person records a transaction and approves the journal entry, the most basic check against error and, in a worst case, fraud has been removed. Even a two-person finance team can implement meaningful segregation with a clear policy on approval thresholds.

The finance teams that scale most effectively are not the ones with the most sophisticated tools. They are the ones with the most disciplined processes. Tools help, but process is what makes the output trustworthy.

How Proseso-consulting supports your monthly close

If you recognize the gaps described in this article, the most direct path to fixing them is working with a team that has built these processes before.

Proseso-consulting provides CFO advisory services for SMEs in Singapore and the Philippines, including close process design, control implementation, and financial reporting setup. The firm’s bookkeeping services and payroll services integrate directly with the closing workflow, so your transaction data is complete and correctly coded before the close window opens. For SMEs that need structured financial oversight without a full-time CFO, Proseso-consulting’s fractional advisory model delivers the process discipline and reporting quality that growing businesses require. Contact Proseso-consulting to discuss how these services apply to your specific close cycle and compliance requirements.

FAQ

What is the 7-step monthly closing process for SMEs?

The 7-step monthly closing process covers pre-close preparation, transaction capture, reconciliations, adjusting entries, account review, approvals with period lock, and a post-close retrospective. Each step produces defined outputs that make the process repeatable and audit-ready.

How long should a monthly close take for a small business?

Most SMEs can complete an effective monthly closing within five to seven business days of the period end. Businesses that track close cycle time and run post-close retrospectives consistently reduce this number over time.

Why is a period lock important in the monthly closing process?

A period lock prevents any changes to approved financial data without documented authorization, preserving the integrity of the audit trail. Without it, figures can shift after approval, making reported financials unreliable.

What are the most common mistakes in SME monthly closing?

The most frequent issues are inconsistent cutoff enforcement, unsupported adjusting entries, and unclear task ownership. Each of these is preventable with a published close calendar, an evidence requirement for every journal entry, and a single assigned owner per task.

How does monthly reconciliation improve financial reporting for SMEs?

Monthly reconciliation steps verify that every balance sheet account matches its supporting source document, catching errors before they flow into the income statement or tax filings. Consistent reconciliation is the foundation of accurate financial reporting for SMEs.

Can SMEs really automate the monthly close?

Yes. Modern accounting platforms — Odoo, Xero, QuickBooks Online — now offer automation across the close: AP bill capture with OCR and AI, direct bank feed integrations, suggestive reconciliation, AR follow-ups, and scheduled recurring entries. Automation does not replace the 7-step framework. It changes how each step is executed, removing manual effort from work that does not require judgment.